Gmbh Und Co Kg Gewinnverteilung

GmbH & Co. KG Gewinnverteilung: What is it and how does it work?

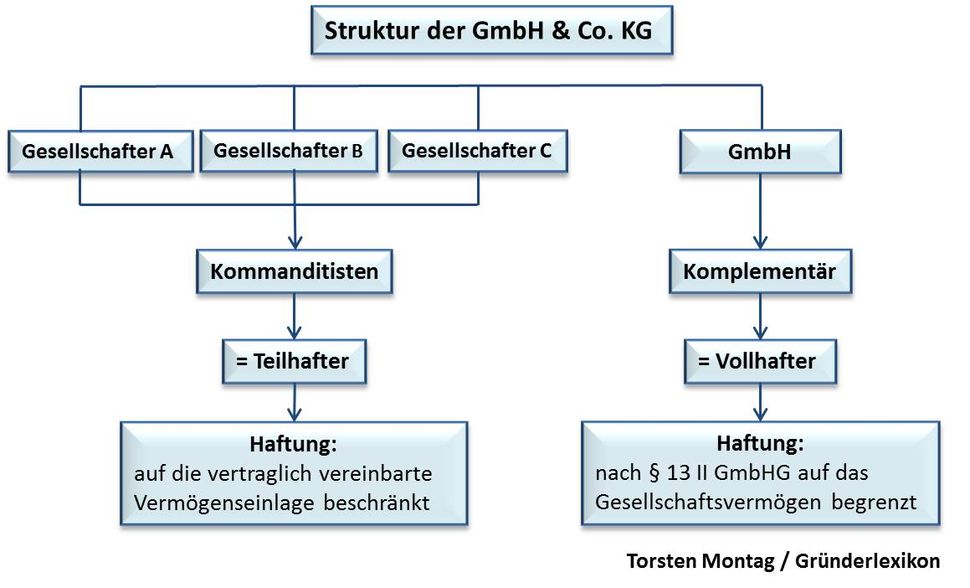

The GmbH & Co. KG is a special type of German company. Think of it as a mix of two types: a GmbH (limited liability company) and a KG (limited partnership). This setup influences how profits are split. The core idea is to fairly divide the profits between the various parties involved.

Step 1: Understanding the Players

To understand the profit distribution, you need to know the roles:

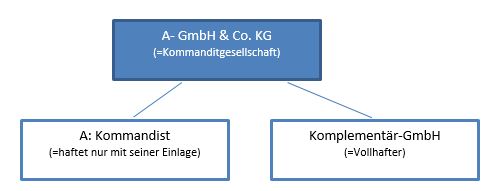

- GmbH (Komplementär): The general partner. This company (the GmbH) has full liability for the KG's debts. Think of it as the manager with all the responsibility.

- KG (Kommanditisten): The limited partners. They have limited liability, meaning they are only liable up to the amount of their contribution. They are more like investors.

Step 2: The Profit Distribution Key (Gewinnverteilungsschlüssel)

The profit distribution key is the agreement on how profits will be divided. This is usually stated in the company's partnership agreement (Gesellschaftsvertrag). It's crucial and should be clearly defined!

Step 3: The Fixed Interest (Vorabgewinn)

Often, the GmbH (the general partner) receives a fixed interest payment (Vorabgewinn) before the remaining profits are split. This is like a salary for taking on the full liability. Imagine the GmbH gets 5% of the total profit right off the top, regardless of the overall success.

Example: Let’s say the GmbH & Co. KG makes a profit of €100,000. The agreement states the GmbH receives a 5% fixed interest. The GmbH gets €5,000 (€100,000 x 0.05) before anything else is distributed.

Step 4: Splitting the Remaining Profit

After the GmbH's fixed interest, the remaining profit is divided according to the partnership agreement. This can be a simple percentage split based on capital contributions or a more complex formula.

Example (Continuing the previous example): After the GmbH's €5,000, there's €95,000 left. The agreement says this is split 60/40 between two Kommanditisten. One gets €57,000 (€95,000 x 0.6) and the other gets €38,000 (€95,000 x 0.4).

Step 5: Allocation to Capital Accounts

The individual shares of profit are usually credited to the partners’ capital accounts. This increases their capital stake in the company. Conversely, losses reduce the capital account.

Example: The Kommanditist who received €57,000 would have that amount added to their capital account balance.

Key Considerations:

- Losses: The profit distribution key also applies to losses! Everyone shares the burden according to the agreement.

- Amendments: The profit distribution key can be amended, but it usually requires unanimous agreement from all partners.

- Tax Implications: The profit distribution significantly impacts the tax liabilities of both the GmbH and the Kommanditisten. Consult with a tax advisor.

- Clarity is Key: The more precise and clear the partnership agreement regarding profit distribution, the fewer potential disputes will arise.

Simplified Example Recap:

Imagine a GmbH & Co. KG making €50,000 profit.

- The GmbH gets a 10% fixed interest: €5,000.

- Remaining profit: €45,000.

- Two Kommanditisten split the remaining profit 50/50: €22,500 each.

- Each amount is added to their respective capital accounts.

Understanding the GmbH & Co. KG profit distribution is vital for anyone involved in this type of company. It provides clarity on how earnings are shared and helps prevent misunderstandings. Remember to always consult the partnership agreement and seek professional advice when needed.